Explore a selection of ESG related articles from IR Magazine

Northern Europe leads the world for capital market ESG, reveals analysis

Finland is the world’s most sustainable stock market Northern Europe leads the way on ESG among the world’s indices, according to the Morningstar Sustainability Atlas, with Denmark scoring highest on social criteria.

The Netherlands scores highest on governance and Portugal tops the environmental criteria.

Denmark’s high score is driven by top holding Novo Nordisk, which is viewed as a leader within the global pharmaceuticals industry, while the Netherlands’ high position is owed to ASML – an ESG leader within the global semiconductor industry – and ING Group, an ESG banking leader.

Portugal scores well thanks to oil and gas producer Galp Energia, viewed as being on top of emissions, effluent and waste, and utility EDP, which has embraced environmental best practices.

But it’s Finland that ranks as the world’s most sustainable stock market, mainly because of the number of ESG-leading stocks: Nokia – identified as an ESG tech leader – KONE, an ESG leader in the machinery sector, and oil and gas group Neste.

Interestingly, Colombia is the world’s highest-scoring non-European market for sustainability. The US ranks in the fourth quintile of global sustainability leaders because of a number of issues involving Amazon, Apple and Microsoft, and poor governance scores from Facebook and Alphabet, Google’s parent company.

China is last in global ESG rankings due to poor corporate governance among companies like Alibaba and Tencent relative to their global peers.

Other Asian markets like Japan and Korea score poorly on governance due to underperformance from companies such as SoftBank and Toyota in Japan and Samsung in Korea. Taiwan is the top Asian market in terms of sustainability, thanks to TSMC, a global ESG leader.

Hungary is a top-performing emerging market thanks to MOL, considered to be a leader among global oil and gas production companies.

Germany scores well on ESG criteria, with several index constituents – including SAP, Allianz and Siemens – considered to be global ESG leaders. The UK finds itself in the second quintile, with companies like Royal Dutch Shell and GlaxoSmithKline classified as outperformers.

Morningstar analyzed its suite of global equity indexes, representing 97 percent of global market capitalization, to assess the respective ESG criteria of each market.

Asset managers align investments with UN Sustainable Development Goals

Survey shows growing commitment to ESG investments A majority of asset managers and asset owners are beginning to align their investments with the United Nations’ Sustainable Development Goals, according to a survey by BNP Paribas Securities Services.

The survey of 347 institutional investors – 178 asset managers and 169 asset owners – shows a growing commitment to ESG investments, with 75 percent of asset owners and 62 percent of asset managers holding 25 percent or more of their investments in funds incorporating ESG criteria compared with 48 percent and 53 percent, respectively, in the previous survey in 2017.

This trend looks set to continue, with 90 percent of investors interviewed by the French firm saying more than 25 percent of their funds will be allocated to ESG investments by 2021.

According to the respondents, ESG data remains the biggest barrier to incorporating more ESG factors into the investment process – as was the case in 2017. Other barriers cited include costs associated with ESG integration, a lack of advanced analytical skills and the risk of managers falsely stating their investment is green.

One third of all respondents also say technology costs are a barrier to ESG integration – up from 16 percent in 2017.

Sixty-six percent of respondents say data is the main challenge when addressing ESG investments, while 32 percent think technology is a key challenge and 30 percent cite the risk of not having the necessary analytical skills.

Only 2 percent of respondents rank improved long-term returns in their top three reasons for ESG investment, though 60 percent of all respondents expect their ESG portfolios to outperform over the next five years.

‘ESG investment is becoming increasingly important for investors, and our survey highlights their appetite to pursue both purpose and performance,’ says Florence Fontan, head of asset owners at BNP Paribas Securities Services, in a statement.

‘But practical integration has its challenges due to data and technology barriers, and deep ESG investment is still finding its feet. The next two years will be critical to achieving the right investment mix, technology and skills.’

BlackRock launches ESG-transparent ETFs

Funds allow investors to apply ESG considerations In a novel ESG investing approach, asset management behemoth BlackRock has launched six new ETFs to offer publicly disclosed data on ESG implications for the assets held within each fund.

Launched in Europe, the new funds are aimed at improving ESG transparency by compiling data from MSCI with the ETFs providing an average ESG quality score and an assessment of the carbon intensity of their underlying portfolio.

The six funds are tracked across MSCI indices that examine security criteria to maximize ESG scores, and the ETFs screen out companies with exposure to nuclear weapons, civilian firearms, tobacco, thermal coal and oil sands and those violating UN Global Compact principles. The funds use MSCI’s methodology to offer a lower-emissions intensity, with MSCI ranking companies on stock exchanges based on their carbon footprint. MSCI then excludes the top 20 percent by emissions intensity from the index.

BlackRock’s vice chairman Philipp Hildebrand says in a statement: ‘Europe is at the forefront of the sustainable investment movement. Across the region, sustainable investing is believed to be the future of investing and many European clients are pursuing the twin goals of addressing the world’s societal and environmental needs while generating the long-term risk-adjusted returns needed to fulfill their financial goals.’

BlackRock hopes the disclosures will help investors make better ESG-related investment decisions. ‘Our Sustainable Core ETF range is about setting a global catalyst for choice and transparency that allows investors to apply ESG considerations to the foundation of their portfolios,’ adds Carolyn Weinberg, global head of iShares at BlackRock. BlackRock predicts the European ETF market for ESG assets will grow from $12 bn today to $250 bn by 2028, representing 60 percent of the estimated $400 bn global market for the funds.

Stephen Cohen, EMEA head of iShares at BlackRock, adds: ‘The way portfolios are built in Europe is undergoing an upheaval, with investors demanding more when it comes to transparency, value and choice.’

A study from Greenwich Associates also finds that half of European institutional investors expect to have more than 50 percent of their assets linked to ESG criteria by 2024.

Related session at the Global IR Forum in Paris

How can you incorporate quant investors and exchange traded funds into your IR strategy? As index-trackers and quant investors increase in importance, we explore third-party databases, index inclusion policies and evaluation metrics to better understand the dynamics of so-called ‘passive investing’ and what IROs need to be thinking about outside of ‘the equity story’, research coverage and earnings calls or meetings with management.

Find out more about the global forum here.

Earnings calls increasingly mention plastic waste

Sustainable investing has a long way to go but companies urged not to fight regulation on plastic Investors are looking deeper into company ESG performance, with MSCI suggesting that firms’ use of plastic is coming under greater scrutiny.

The mention of plastic waste in earnings calls increased by 340 percent in 2018, compared with the previous year, according to MSCI research. The index provider predicts that 2019 will see many organizations forced to deal with the reality that their investors view excessive use of plastic as a business risk.

The disruption stems largely from a changing regulatory landscape pushing companies to deal with waste reduction. China first pulled out of the thriving global trade in waste in early 2018, then the European Parliament voted in the same year to ban single-use plastic by 2021, including a requirement to recycle more than 90 percent of beverage bottles by 2025. And California was the first state to introduce a ban on single-use plastic bags at large retail stores in 2014. According to the United Nations, plastic has caused $8 bn worth of damage to the world’s marine ecosystem.

Conrad MacKerron, senior vice president of As You Sow, a non-profit foundation chartered to promote CSR through shareholder advocacy, notes that no organization is immune to investment and reputational risk. He tells IR Magazine: ‘Firms with ESG investors understand that [plastic] presents a risk to their brand.’

Reputational hazard

But MacKerron adds that not all investors are up to speed with the focus on plastic. ‘It’s a wasteful throwaway [business] culture where we have single-use plastic that’s used for just a few minutes or seconds and thrown away,’ he says. ‘And some investors are behind on some of these concerns.’

Tatiana Luján, wildlife conservation lawyer at ClientEarth, a non-profit environmental law organization, predicts that the use of plastic will be ‘more and more’ regulated and companies will not have enough time to adapt and change their ways of production and distribution.

‘To overcome these risks, businesses should involve the public because if this isn’t managed, they will face reputational risks,’ she notes. ‘The way companies differentiate themselves is in their branding, which is a very large part of their capital. If their brand is found to be associated with plastic pollution or with chemicals that leak from plastic, their corporate value is going to be at risk. So they should engage with the public and be more transparent.’

She says there are a lot of organizations that are thinking about investments in the long-term to deal with the plastic shutdown. The Coca-Cola Company, for example, tells IR Magazine that it is looking into how it can make a positive impact on the plastics problem within oceans and landfills.

Investor questions on plastic up 30 percent The firm’s senior investor relations manager Nick Johnson says that in addition to the company launching its World Without Waste initiative, which plans on collecting and recycling a bottle or can for each one it sells by 2030, it has identified that non-ESG investors are taking the issue seriously.

Johnson says investors are now looking through an environmental lens at how they go about investments. ‘Investors want a culture change because they understand that plastic pollution is not just a Coke problem but a global issue,’ he explains. ‘The conversation on plastic went from not coming up in meetings with equity and debt investors to it probably coming up 30 percent of the time. That’s a pretty big increase.’

Research by UK retailer Marks and Spencer Group finds that a large number of the questions it receives on plastic and ESG are consumer-led. The firm was clear to IR Magazine that plastic has always been on its agenda but the issue has now accelerated because of what is happening externally.

‘Our investor base is becoming a lot more engaged in broader corporate sustainability responsibility and governance goals, of which plastic is one,’ says Rebecca Edelman, M&S’ investor relations manager.

The retailer plans to be a zero-waste business by 2025. ‘We want to use plastic only where there is a clear and demonstrable need,’ Edelman adds. ‘We are aiming to remove 1,000 tons of plastic packaging by spring this year.’

Don’t fight the regulation With regulation coming in steady drips, shareholders have to build up their knowledge – otherwise their investment is at risk. ‘Investors need to take practical steps in the companies they are shareholders of. They must not fight the regulation,’ Luján advises.

Johnson says this is already happening at Coca-Cola, where some investors are pushing for information around several environmental and social issues. ‘The investors are skeptical but they want to know much more about what we’re doing around plastic, water and sugar,’ he says. ‘They want to know what we’re doing as a good global steward, what sort of investment will be required and what that means to their overall investment in the company.’

One way to push the plastic agenda along and keep investors happy is to listen to the people who buy the products, suggests Dustin Stilwell, head of investor relations at Berry Global. He says the key focus for the business is to meet customer requests, so if they want more recycled content, the business makes sure it delivers.

Taking this approach means Stilwell spends some time reassuring investors their customers will follow them on their journey to think more carefully about the use of plastic. ‘Our investors really want to know whether [our customers] will be OK with any type of price differential,’ he notes.

Nintendo Switch success drives governance questions

Development highlights remaining questions around Japanese corporate governance Nintendo’s share price is at a near-10 year high, topping ¥48,000 ($449) – but the company faces questions over its corporate governance.

The boost to the Kyoto, Japan-headquartered company’s stock comes off the back of the huge success of its Switch console, which has sold more than 12 mn units since its launch in March last year. But its success is pricing out many retail investors because of a minimum trading limit of 100 shares, with both CNBC and the Financial Times reporting that some investors are calling for a stock split to widen the shareholder base and aid governance.

The FT quotes Macquarie analyst David Gibson as saying a stock split would be ‘a good first step’ toward greater transparency, while on CNBC Atul Goyal of Jefferies discusses the governance implications of such a move.

According to data from Morningstar, the firm did split its stock once, in 1989, with a 3:2 ratio.

‘Nintendo is notorious for bad IR,’ Hitoshi Sugibuchi, representative director at governance and IR consultant Sessa Partners, tells IR Magazine. ‘Nintendo does not attend brokers’ conferences, doesn’t do overseas roadshows or even conference calls. It accepts meetings only with investors that come to its headquarters in Kyoto, and then with a limited time window.’

A request for comment from Nintendo was not returned within 24 hours. This article will be updated with comments if received.

There are signs the firm is becoming more transparent, however. In his most recent statement to shareholders, company president Tatsumi Kimishima announced plans to widen access to Nintendo’s intellectual property with plans for everything from gaming cards to theme parks and a new Mario film being made with Illumination Entertainment, the US film and animation studio behind Despicable Me.

‘Not many investors criticize Nintendo because of its unique business domain,’ Sugibuchi continues. ‘Although gaming is a large industry, the business culture and management style is quite different compared with other sectors. The drivers are creators and engineers whose incentives are interest and curiosity rather than money. Nintendo has created its own management way and operational policy, and many investors respect this even though some complain about poor disclosure.’

Governance review

Japan introduced a new corporate governance code in 2014, but there are concerns that governance has remained a box-ticking exercise at some firms. That said, Sugibuchi notes that 98 percent of the JPX-Nikkei 400 now has two or more outside directors, as required by the code. This is an increase from 21 percent before the code came into force.

Outside directors are not having the desired impact at Japanese companies in general. ‘High levels of retained cash in company balance sheets, low dividend-payout ratios and a slow pace on the unwinding of cross-shareholdings [where the company owns shares in a partner firm]’ are all adding to these concerns, Sugibuchi adds. ‘The first step in the introduction of outside directors is over,’ he says. ‘Our focus from now on is how outside directors work, monitoring the board and even confronting the CEO if necessary.’

Japan’s Financial Services Agency (FSA) is now preparing to revise and strengthen the existing code, which also allows companies to switch to a new governance structure by appointing statutory auditors as outside directors.

This is something Nintendo has taken advantage of, with all three of the firm’s outside directors having previously served as Nintendo auditors. Such individuals would not be considered independent directors in other jurisdictions, and their appointment is therefore unlikely to impress foreign investors. Sugibuchi notes that such moves are little reported on within Japan, partly because the practice is allowed under the code but also because, even in the media, there is ‘not a good understanding of corporate governance.’

The FSA is expected to publish its draft statement for changes to the code in June, with CEO performance, appointment and termination among other issues on the agenda. But Sugibuchi says it is companies’ philosophy that needs to change. ‘Traditionally, Japanese people respect seniority,’ he explains. ‘Thus, CEOs have strong leadership and board members will not strongly oppose them. But board members should understand that they work for the shareholders, not the CEO.’

The role of investors

As well as the introduction of the corporate governance code, 2014 also saw the FSA introduce a stewardship code to promote greater dialogue between investors and companies and push for governance reform – but again, progress has been slow.

‘There wasn’t much improvement in terms of the relationship between the buy side and companies in the first few years,’ Sugibuchi notes. In a renewed push last year, the government called on asset management firms to disclose their voting records at annual meetings, something the majority of asset management firms have now begun to do.

Japan’s Government Pension Investment Fund (GPIF) – the world’s largest pension fund with assets of around ¥162.67 tn as of September 2017 – has been increasingly focusing on governance. It does not invest directly in equities but via asset managers and ‘in order to improve productivity in the private sector, GPIF is demanding that asset managers build engagement with corporate management,’ says Sugibuchi. ‘It has a strong influence in the investment world, and its current focuses are corporate governance and ESG.’

In July 2017 MSCI launched two new ESG-focused indexes aimed at Japanese companies: the MSCI Japan Empowering Women Index and the MSCI Japan ESG Select Leaders Index, with the GPIF.

The country is also seeing a slight increase in shareholder activism, Sugibuchi adds. For example, GPIF has invested in Taiyo Pacific, a US activist fund targeting Japanese companies. Still, ‘Japanese institutional investors are reluctant to ally with aggressive foreign investors,’ Sugibuchi says, adding that if a campaign became a proxy fight at the AGM, ‘it seems unlikely minority shareholders could beat company management without teaming up with domestic investors.’

He says public campaigns are likely to have more of an impact as Japanese management values reputation.

Governance briefing: The changing nature of disclosure, transparency and shareholder rights This year has seen a surge in corporate governance-related reforms and advocacy efforts across many markets. We examine the collective direction of these reforms and what IR can do to stay ahead of a growing trend in governance.

IR Magazine Global Forum & Awards The biggest global gathering of IR professionals Paris, October 2-3

The ESG Integration Forum – Europe ESG: From trend to action London, November 7

The ESG Integration Forum – US Proactively responding to ESG expectations New York, December 5

SSGA's ESG data challenge

While many investors are looking at ESG as a screen for long-term value creation, Rakhi Kumar and Ali Weiner outline the challenges they face in getting objective and accurate ESG data Quality data about companies’ ESG practices is critical for effective investment analysis. The lack of standardization and transparency in ESG reporting and scoring presents major challenges for investors. Third-party ESG data providers play an important role, but there are limitations with this data – especially in terms of differing methodologies that lead to variance in scores – that asset owners should understand.

Moreover, there is a lack of market infrastructure that can give companies insights into how they are evaluated with respect to ESG scoring. To improve the quality of the ESG data we use to make investment decisions for our clients, State Street Global Advisors (SSGA) has built a scoring system that uses data from multiple best-in-class providers, leverages the SASB transparent materiality framework and incorporates our stewardship insights.

Here, we outline the considerations asset owners should incorporate into their evaluation of ESG data providers.

Headwinds to ESG data quality

Quality data is the lifeblood of investment analysis. While ‘quality’ can be defined in several ways, most investors agree that consistency and comparability in the availability of data across companies are essential elements of an effective dataset.

Unfortunately, the current landscape provides headwinds to achieving those elements of quality when it comes to data about a company’s ESG practices. Governments around the world don’t require companies to report on most ESG data so companies are left to determine for themselves which ESG factors are material to their business performance and what information to disclose to investors.

Asset owners and their investment managers seek solutions to the challenges posed by a lack of consistent, comparable and material information. Investors increasingly view material ESG factors as being critical drivers of a company’s ability to generate sustainable long-term performance. In turn, ESG data has increasing importance for investors’ ability to allocate capital in the most effective manner possible.

ESG data providers play an important role in the investment process by gathering and assessing information about companies’ ESG practices and then scoring those companies accordingly. The development of these ratings systems has helped to nurture the growth of ESG investing by giving asset owners and managers an alternative to conducting such extensive diligence themselves.

As of 2016, there are more than 125 ESG data providers, according to the Global Initiative for Sustainability Ratings. These include well-known providers with global coverage such as Bloomberg, FTSE, MSCI, Sustainalytics, Thomson Reuters and Vigeo Eiris, as well as specialized data providers such as S&P’s Trucost (providing carbon and ‘brown revenue’ data), GRESB (sustainability performance in real estate) and ISS (corporate governance, climate-related and responsible investing solutions).

Despite the valuable contributions these data providers have made in advancing ESG investing globally, it’s important for asset owners and managers to understand the inherent limitations of this data, as well as the challenges of relying on any one provider.

Differences in data collection and methodologies

Lack of standardization and transparency in providers’ data collection and scoring methodologies pose key challenges for investors. ESG data providers generally develop their own sourcing, research and scoring methodologies.

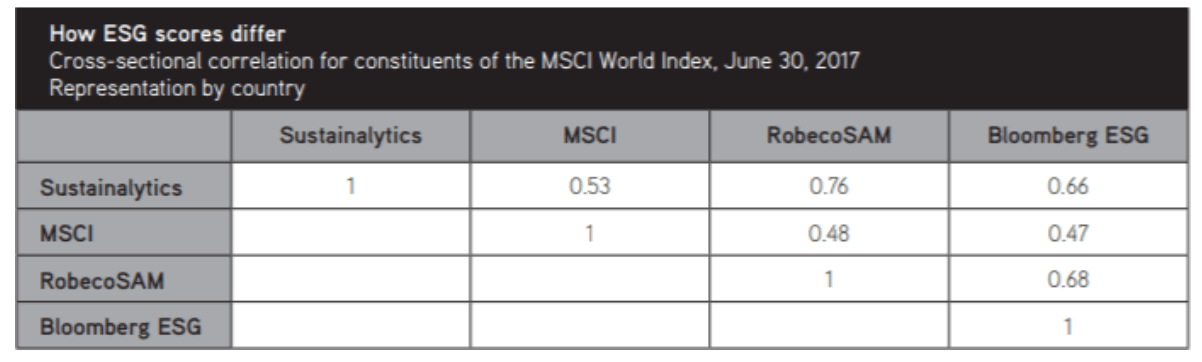

As a result, the rating for a single company can vary widely across different providers. We recently conducted research to quantify the degree to which this lack of standardization leads to variance among the ESG scores used by investors.

As part of an 18-month due diligence process in which we looked at more than 30 data providers, we examined the cross-sectional correlations for four leading data providers’ ESG scores, using the MSCI World Index as the coverage universe. MSCI and Sustainalytics are two of the most widely used ESG data providers. But, as shown in How ESG scores differ, our research determines a correlation of only 0.53 among their scores, meaning that their ratings of companies are only consistent for about half of the coverage universe.

These differing methodologies have implications for investors. In choosing a particular provider, investors are, in effect, aligning themselves with that particular company’s ESG investment philosophy in terms of data acquisition, materiality, aggregation and weighting. This choice is complicated by the lack of transparency into those methodologies. Most data providers treat their methodologies as proprietary information. By relying on an ESG data provider’s score, therefore, asset owners are taking on the perspectives of that provider without a full understanding of how it arrived at its conclusions.

Assessing the differences

Given the lack of consistency in ESG scores, it’s helpful to understand the factors that are leading to this variance. In our research, three primary points of difference among the methodologies and approaches used by ESG data providers are identified, as follows.

Materiality – A critical part of any ESG scoring is determining which factors are material to a company’s financial performance. As part of the proprietary nature of their solutions, ESG data providers typically make their own determinations on materiality issues – and don’t provide full transparency into how these determinations are made. These differences in how materiality is defined and unveiled add to the difficulty asset owners and managers face in selecting an ESG data provider.

Data acquisition and estimation – We found discernible differences in how ESG data providers source and acquire raw data. In addition to using traditional sourcing techniques to gather data that is disclosed by the company or otherwise publicly available, ESG data providers use statistical models to create estimates for unreported data. These models are based on averages and trends at what the data provider views as similar companies and industry benchmarks. This is an example of how investors are unwittingly incorporating judgment calls by the data provider into their investment decision-making processes.

Aggregation and weighting – Each ESG data provider has developed its own method to aggregate and weight particular ESG factors for its summary scores. Again, these are proprietary judgments made by each individual provider.

ESG scoring at State Street Global Advisors (SSGA)

We believe ESG factors are directly linked to a company’s ability to generate sustainable long-term performance. As fiduciaries, we have a duty to rigorously analyze all financial and non-financial factors that can affect a company’s performance, and we believe ESG factors can be used to mitigate risk and identify potential alpha signals.

To address the gaps in the current market infrastructure, we are building our own scoring system, known as R-Factor. This scoring system will address the data challenges we’ve articulated in these pages. Our approach to ESG data and scoring is guided by three goals:

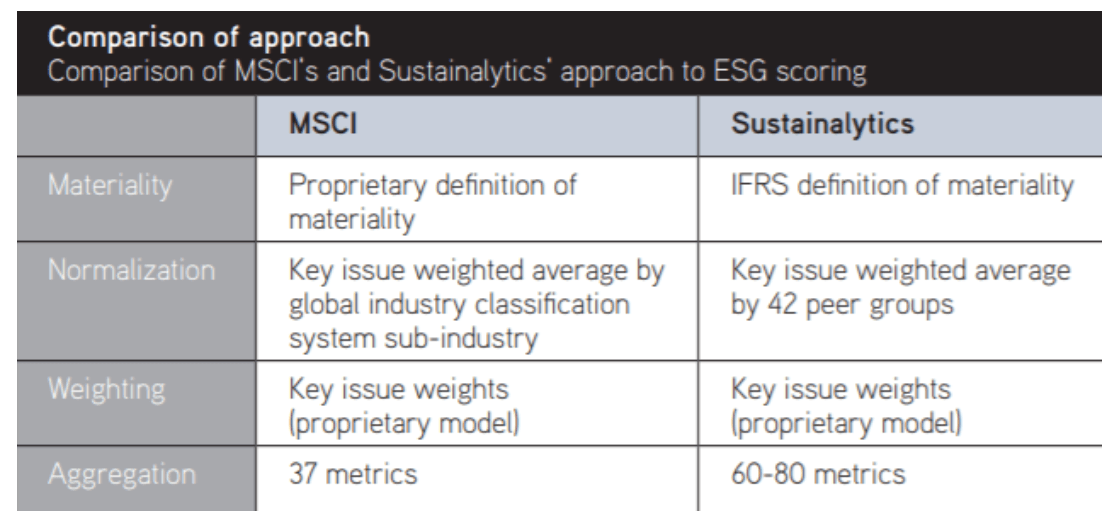

Case study: MSCI versus Sustainalytics

Both MSCI and Sustainalytics are widely used across the asset management industry, and each of them offers global ESG product suites, including ESG ratings and climate-focused products. As Comparison of approach (below) illustrates, however, there are distinct differences in the way the two firms collect and analyze ESG data.

This article appeared in Corporate Secretary’s special report on ESG engagement, reporting and integration

What research is unearthing about ESG

A roundup of ESG research from the academic world, as collected by Jeff Cossette Mounting evidence confirms companies can ‘do well by doing good.’ Now researchers are digging deeper into the nuances of that relationship and discovering the need to distinguish between different types of sustainability practices.

A key question facing boards today is whether sustainability amounts to a differentiating strategy leading to competitive advantage or a practice bound to spread through imitation and thus important for corporate survival but not necessarily linked with industry outperformance.

Now comes new research that reveals companies tend to adopt an increasingly similar set of sustainability practices and only firms implementing strategic practices – those less common, more differentiated and difficult to imitate – can reliably hope to achieve superior performance.

‘Over time, most industries see the convergence of best practices,’ observes Ioannis Ioannou, associate professor of strategy and entrepreneurship at London Business School. ‘That’s important for corporate survival and legitimacy. But our results show that companies that adopt the less common sustainability practices are most likely to outperform.’

Analyzing data from MSCI ESG ratings from 2012 to 2017, Ioannou and his study co-author George Serafeim, professor of business administration at Harvard Business School, find that adopting strategic sustainability business practices is significantly and positively associated with both return on capital and expectations of future performance as reflected in price-to-book valuation multiples – whereas assuming the more common sustainability practices correlates only with expectations of future performance.

‘Boards need to monitor trends in their industry to help determine the sorts of practices that can be the foundation for their competitive advantage,’ says Ioannou. ‘And they must also consider that what is strategic today may well become common tomorrow. To stay ahead of the pack you need to be continuously looking for those strategic initiatives that would be hard to diffuse throughout an industry.’

Catastrophe, groupthink and the case for board ethnic diversity Regulators, investors and diversity advocates have argued that ethnic diversity may strengthen board monitoring. But the first empirical investigation of the issue suggests the domain of debate may need to shift.

‘Women directors have been shown to strengthen monitoring and I expected [similar results] with ethnic minorities,’ says study author Paul Guest, professor of corporate finance at King’s College London. ‘But I didn’t find this at all.’

Sampling 15 years of S&P 1500 data, Guest explores a range of board-monitoring outcomes including CEO compensation, CEO turnover, performance sensitivity, accounting misstatements, acquisitions and performance. He finds ethnicity has no impact on oversight or performance.

‘If you are going to argue [for ethnic diversity], you must make the case on moral grounds,’ concludes Guest. ‘You can’t argue that the company’s performance will improve – because it doesn’t.’

The corporate governance drivers of ESG disclosure The first meta‐analysis of evidence on corporate governance’s effect on ESG disclosure has clarified which mechanisms best improve communications. Study results show board independence, size and female directorships significantly enhance voluntary disclosure while board ownership and CEO duality have either no influence or a slightly negative one.

Study co-author Nicola Cucari, research fellow at the University of Salerno, says the findings underline the board’s profound influence on ESG disclosure. ‘Unique human competencies and organizational strategies create sustainable competitive advantages for companies,’ he notes. ‘But identifying appropriate corporate governance practices is still a challenge and the ideal board structure remains a question with no universal answer.

‘Outward-facing corporate secretaries able to complement financial with non-financial information can play an important support role in the [ESG disclosure process].’