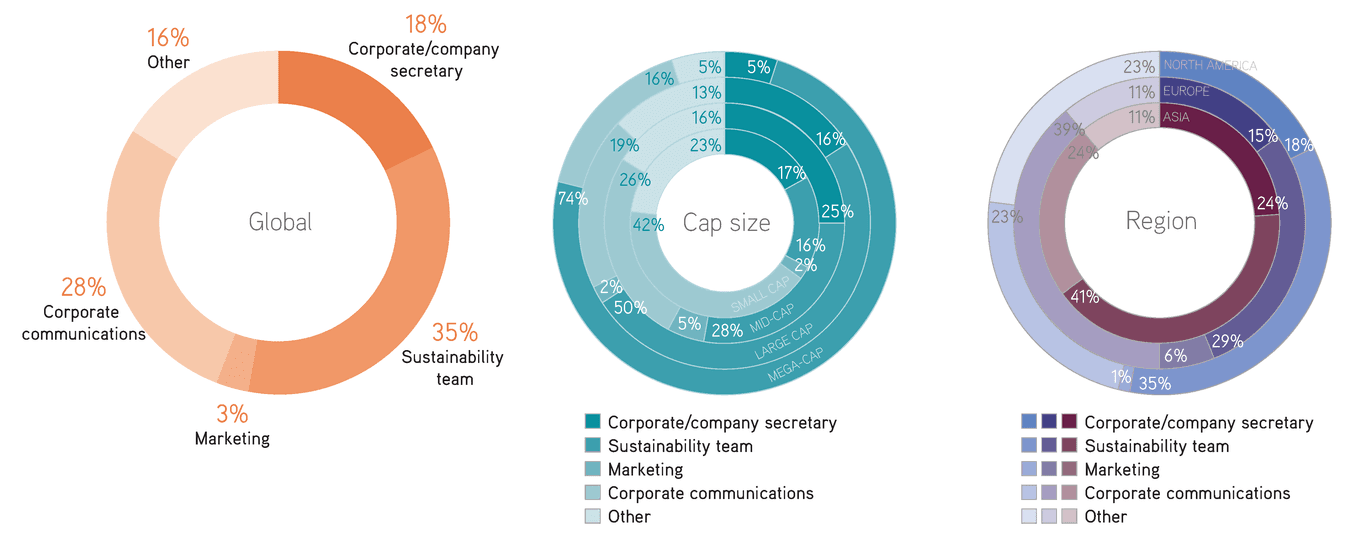

Who is responsible for ESG reporting?

Primary responsibility for ESG communications rests with a dedicated sustainability team at more than a third of companies polled, while responsibility lies with corporate communications at a further 28 percent. Regionally, the practice of the sustainability team having primary responsibility for ESG communications is most prevalent in Asia, with 41 percent doing so. In Europe it is more common for corporate communications to take the lead, with 39 percent of firms assigning primary responsibility to this department. ESG communications responsibility changes according to company size: just 16 percent of small-cap companies have a dedicated sustainability team responsible for ESG communications. This rises steeply as company size increases to the point where almost three quarters of mega-cap companies give responsibility to the sustainability team. At the same time, corporate communications responsibility for ESG communications drops from 42 percent among small-cap companies to 16 percent at mega-caps.

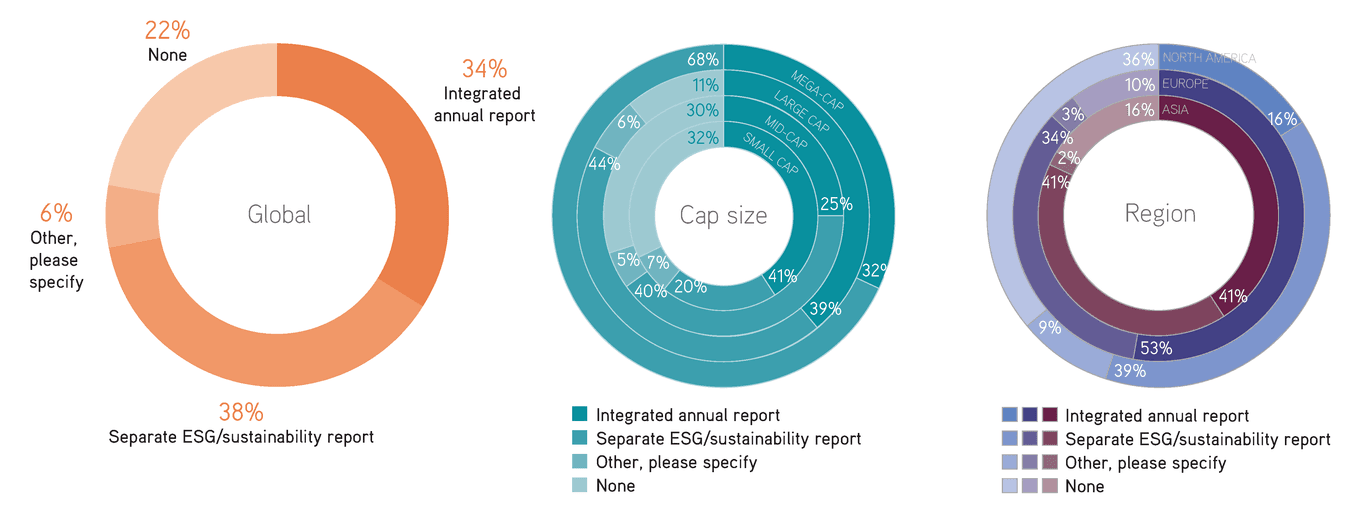

Having a separate sustainability report is the most common means of ESG reporting. Overall, 38 percent of companies report in this way, compared with 34 percent that integrate their ESG reporting into their annual report. More than a fifth (22 percent) of companies do not formally report on ESG issues. ESG reporting is least common in North America, where 36 percent have no formal reporting structure, while in Europe nine in 10 companies report on ESG issues. Europe also sees more firms report in an integrated manner, rather than having a separate ESG report. Producing a stand-alone ESG report becomes more common the larger the company. One in five small-cap companies have a separate ESG report, rising to 68 percent of mega-caps. Similarly, larger companies are more likely to report on ESG in general: more than three in 10 small or mid-cap companies fail to report on ESG at all, while 89 percent of large-cap companies and all mega-cap firms surveyed have a formal reporting process for ESG.

Who has primary responsibility for your company’s ESG communications?

What kind of ESG reporting do you conduct?

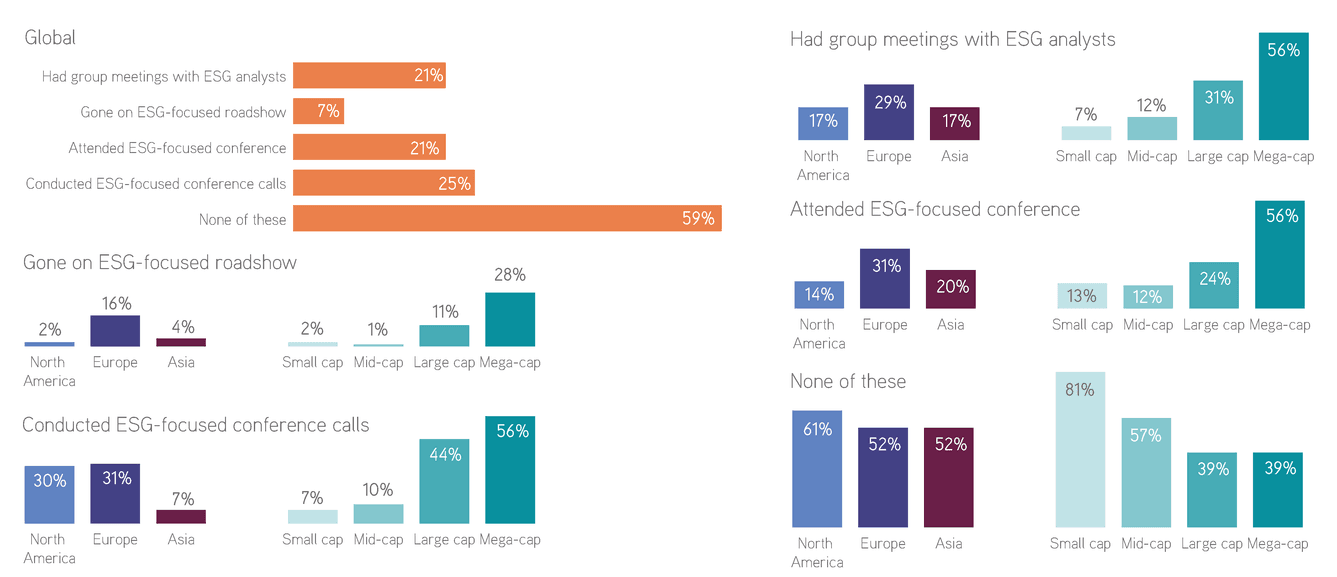

One quarter of IR professionals have conducted an ESG-focused conference call over the past year. This is the most common form of investor engagement on ESG issues, followed by meetings with ESG analysts and attendance at ESG conferences. Just 7 percent of IROs have gone on an ESG-focused roadshow and nearly six in 10 have not undertaken any of these ESG-related investor events in the past year. All of these activities are most common among European IROs. North American IROs prefer ESG-focused conference calls over investor events, while the opposite is true in Asia. ESG-focused investor engagement is more common at larger companies. Between mid-cap and large cap there is a 34 percentage-point jump in the number of IROs holding ESG conference calls. More than eight in 10 small-cap and 57 percent of mid-cap IROs have not engaged in any of these ESG-related activities. This falls to a minority of 39 percent of large and mega-cap IR professionals.

Have you done any of the following over the last 12 months?

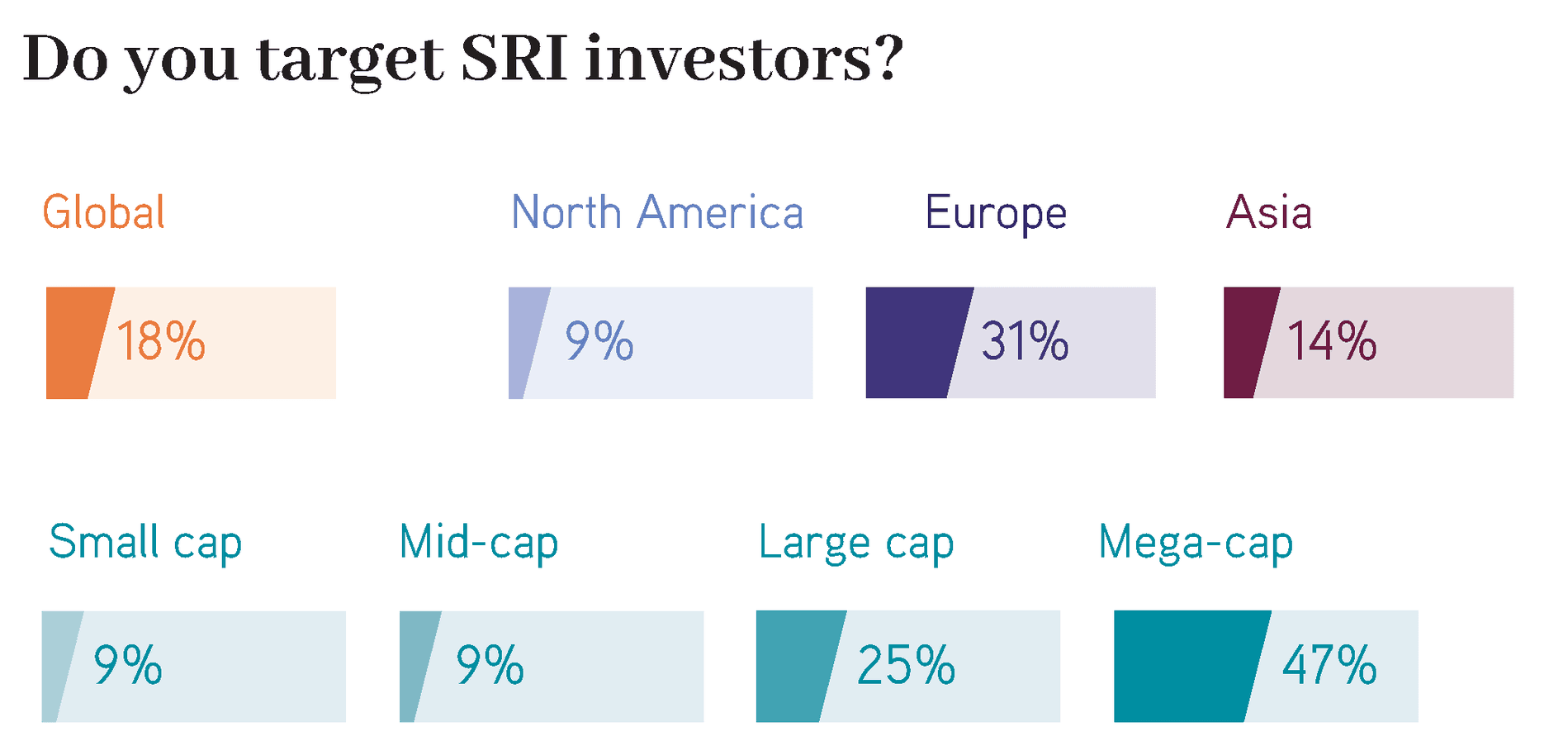

Globally, targeting SRI investors is a niche activity, with just 18 percent of companies actively targeting such investors. But there are considerable regional differences: while fewer than one in 10 North American companies target SRI investors, more than three in 10 European companies do so. SRI investor targeting is an activity commonly seen at larger companies but barely significant for smaller companies: just 9 percent of small and mid-cap companies engage in SRI targeting, rising to 25 percent of large caps and almost half of mega-cap firms.

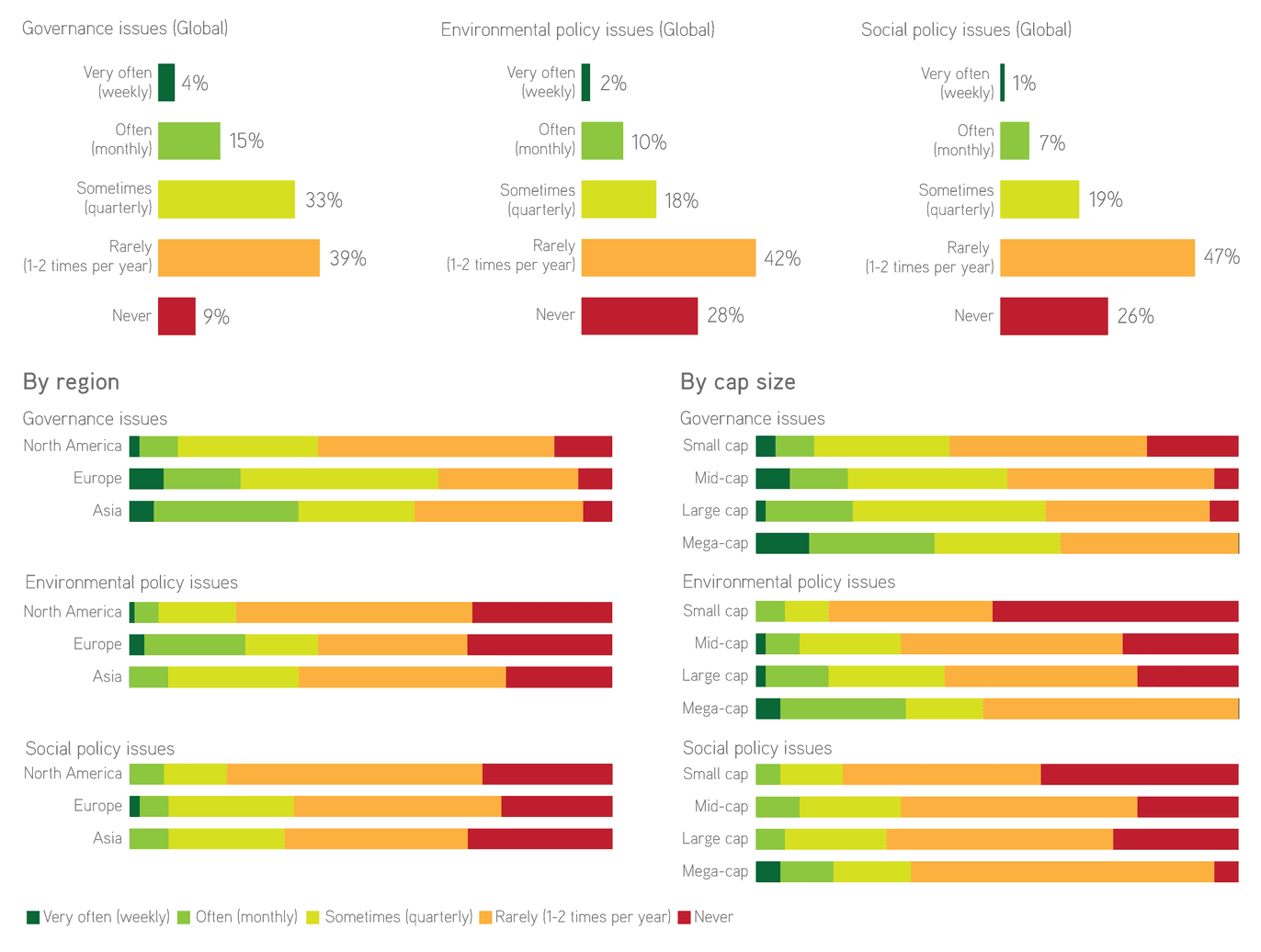

Governance is the issue most frequently discussed with investors. A majority of IROs have at least quarterly discussions with investors about governance, compared with 30 percent who have environmental discussions and 27 percent who have discussions about social impact over the same time period. European IROs are most likely to hold regular discussions on all ESG matters, although it is notable that more than a third of Asian IROs discuss governance with investors at least monthly. Nearly two thirds of European IROs discuss governance with investors at least quarterly, while 80 percent of North American IROs rarely or never hold discussions on social policy issues. Generally, the frequency of discussions on all ESG matters increases with cap size, the only exception being that mid-cap IROs discuss social policy issues marginally more frequently than large-cap and mega-cap IROs. More than half of small-cap IROs never discuss environmental issues with investors and 41 percent of them never discuss social policy issues. All mega-cap IROs have had governance and environmental discussions with investors in the past year, while just 5 percent have not discussed social policy issues.

Governance is also the issue most frequently reported on, with 44 percent of ESG reporting focused on this issue. More time is spent reporting on environmental than on social policy issues, although not to a significant degree. Focus on governance is even greater in North America, where just 23 percent of ESG reporting centers on social policy issues. Asia has a higher focus on environmental and social policy issues than the global norm and therefore a lower focus on governance in ESG reporting.

How often have you discussed the following with investors over the past 12 months?

Separating out E, S and G, what ratio of your reporting is on each (approximate percentage)?

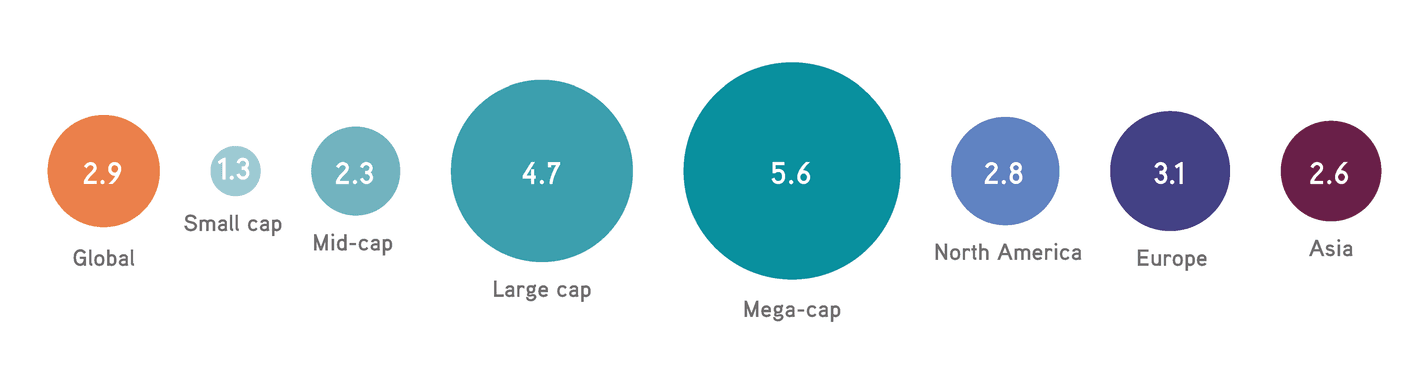

The average number of annual requests from ESG ratings agencies or index providers that IROs respond to is 2.9. Regionally, the average is slightly higher in Europe and slightly lower in Asia. The average number of requests responded to each year rises from 1.3 among small caps to 5.6 at mega-cap level. Globally, 47 percent of survey respondents have participated in a survey from an ESG ratings agency, while 39 percent have checked reports from ESG ratings agencies before publication. Just under half (45 percent) of respondent companies have not engaged in either of these activities over the past year. Regionally, Europeans are more likely to engage with ESG ratings agencies by either participating in a survey or checking reports before publication. Nearly two thirds have undertaken one or both of these activities in the past year.

How many information requests/questionnaires from ESG rating agencies/index providers do you respond to each year?

Survey participation rises with company size: just 13 percent of small caps have undertaken an ESG survey in the past year. This number increases through the cap sizes to 78 percent of mega-caps. Large-cap companies are the most likely to check ESG ratings reports before publication: nearly two thirds have done so in the past year, compared with just 9 percent of small caps. A quarter of IROs never check their companies’ ESG ratings, while 40 percent check them only once or twice a year. Just 11 percent feel the need to check their ESG ratings on a monthly basis. Again, it is Europeans who are most engaged with ESG ratings. While 22 percent of European IROs check their ESG ratings at least monthly, just 7 percent of North American and 8 percent of Asian IROs do the same. Almost half of all small-cap IR professionals never check their company’s ESG ratings. This number falls to just 6 percent for mega-cap IROs, more than a third of whom check their ratings on an at-least monthly basis.

How regularly do you monitor your ESG ratings?

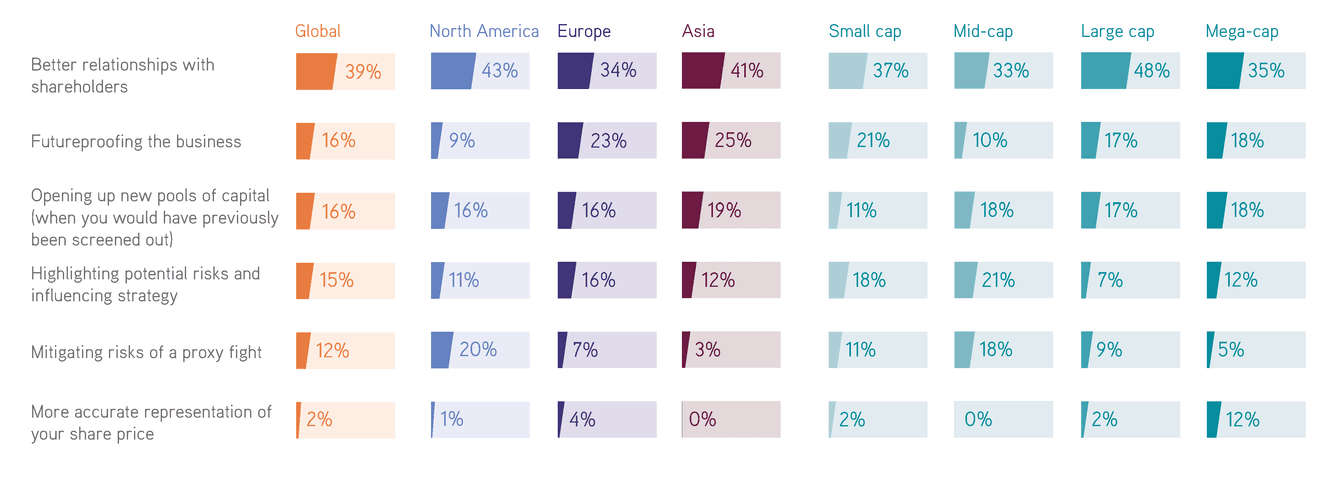

IROs clearly believe ESG adds value to their shareholders. When asked to rank six potential benefits of ESG disclosure, 39 percent cite ‘better relationships with shareholders’ as their first choice, while nearly two thirds have it in their top two. ‘Futureproofing the business’ and ‘opening up new pools of capital’ jointly rank next, followed by ‘highlighting potential risks and influencing strategy’. ‘Better relationships with shareholders’ is the highest-ranked benefit in every region and across every cap size. ‘Futureproofing the business’ is notably more highly valued as a benefit in Europe and Asia than in North America, where ‘mitigating risks of a proxy fight’ is the second-most valued benefit of ESG disclosure; it barely features as a consideration in Europe and Asia. ‘Highlighting potential risks and influencing strategy’ appears to be a more important benefit for smaller companies. ‘Mitigating risks of a proxy fight’ is particularly valued by mid-cap companies, while mega-cap companies favor ‘futureproofing the business’ and ‘opening up new pools of capital’ as the main benefits of ESG disclosure after ‘better relationships with shareholders’.

What are the main benefits of ESG disclosure? Top-ranked choices