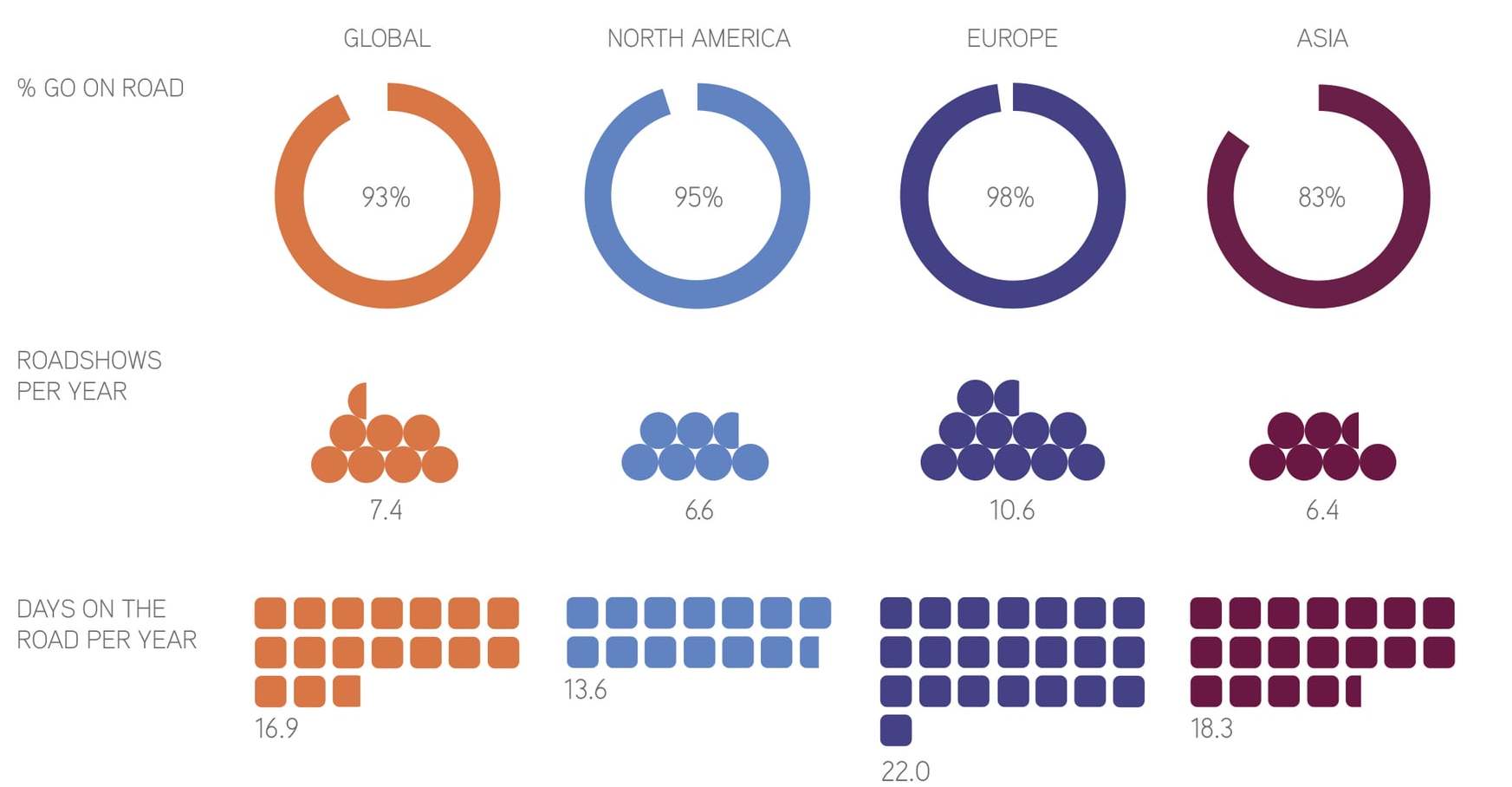

Roadshows remain an essential activity for the vast majority of companies, with 93 percent of companies globally having gone on the road in the past year. Asian companies are less likely to go on roadshows than their North American and European counterparts, with 16 percent staying at home in 2019. Just one in 50 European companies and one in 20 North American companies failed to go on the road in the past 12 months.

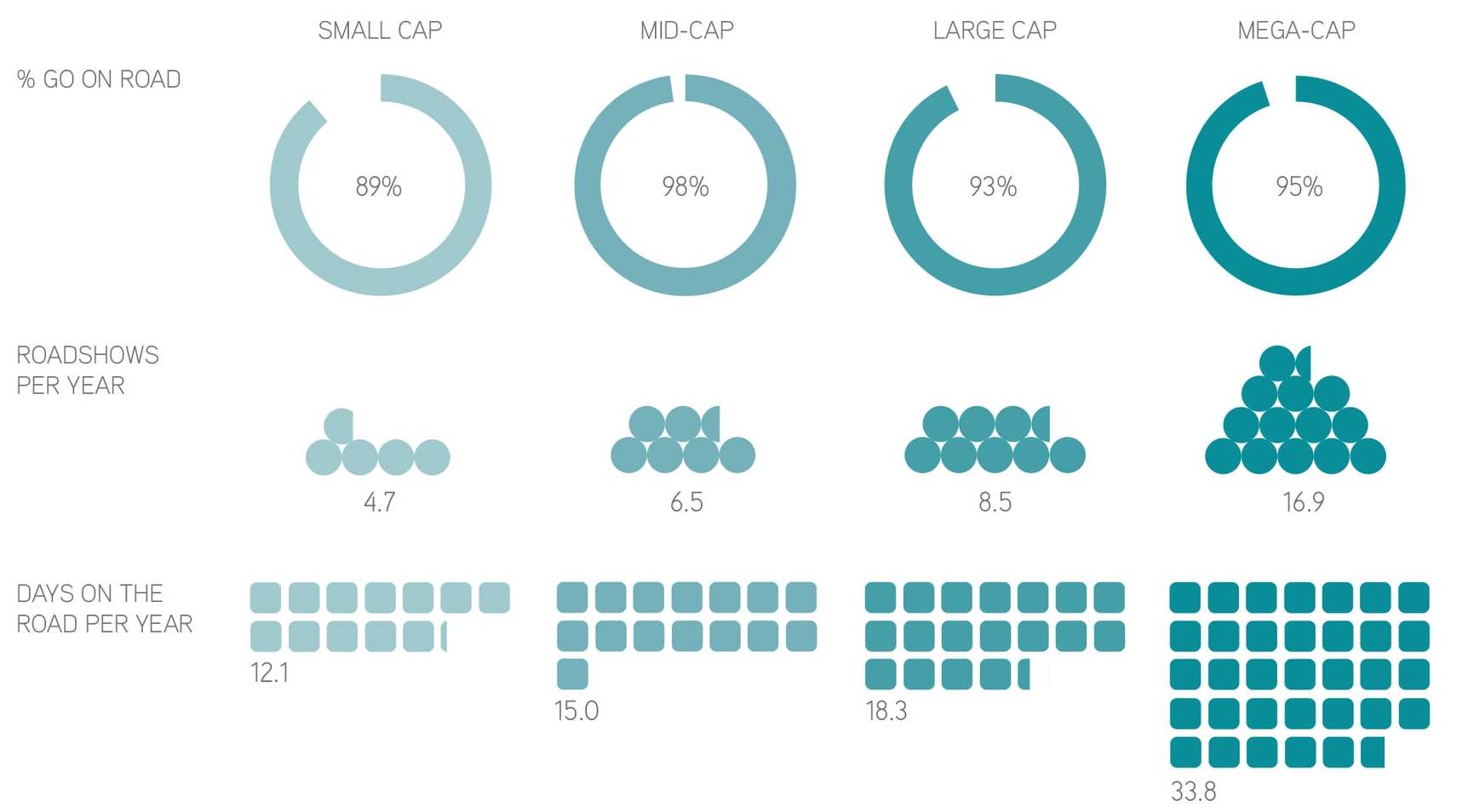

The number of small-cap companies participating in roadshows has increased by just 1 percentage point – to 89 percent – since last year. This does, however, continue the trend seen over the past few years of small-cap companies being increasingly likely to go on the road. Mid-cap and mega-cap companies are the most likely to go on roadshows – at 98 percent and 95 percent, respectively – but the number of large-cap companies on the road has dropped from 97 percent in 2018 to 93 percent in 2019.

Globally, the number of roadshows companies participate in has changed little in the past year. Those who go on the road went on an average of 7.4 roadshows in 2019 compared with 7.5 in the year before.

European companies have added an extra roadshow to their calendar, going from 9.6 in 2018 to 10.6 this year. Asian companies went on an average of 6.4 roadshows in the past year, an increase of 0.7 from 2018. North American companies, however, have seen a decrease in the number of roadshows from 7 in 2018 to 6.6 in 2019.

Looking at the results by company size, the number of roadshows has changed little in the past year from small to large cap: all have seen a marginal drop in roadshow numbers, the largest being a decrease of 0.4 among large-cap companies to an average of 8.5 in 2019. Mega-cap companies are the only cap size to see a notable change in the number of roadshows they undertake, adding an average of 3.5 extra roadshows to take their total from 13.4 in 2018 to 16.9 in the past year.

The number of days companies spend on the road has increased slightly in 2019, with the global average number increasing to 16.9 in the past year, compared with 16.6 in 2018.

As the number of roadshows has increased for European and Asian companies, so has the number of days on the road. European companies have added 3.5 days to their time on the road in the past year, while Asian companies’ days on the road have increased from an average of 17.7 to 18.3. North American companies have lost half a day on the road, going from 14.1 in 2018 to 13.6 in 2019.

The number of days on the road has increased for both small-cap and mega-cap companies in the past year, while decreasing for both mid-cap and large-cap companies. Mega-cap companies have added more than four days to their calendar to spend an average of 33.8 days on the road in the past year, while small-cap companies’ days on the road have increased from 11.4 to 12.1. Large-cap firms have lost a day on the road, going from an average of 19.3 in 2018 to 18.3 in 2019, while mid-caps have gone from 15.6 to 15.

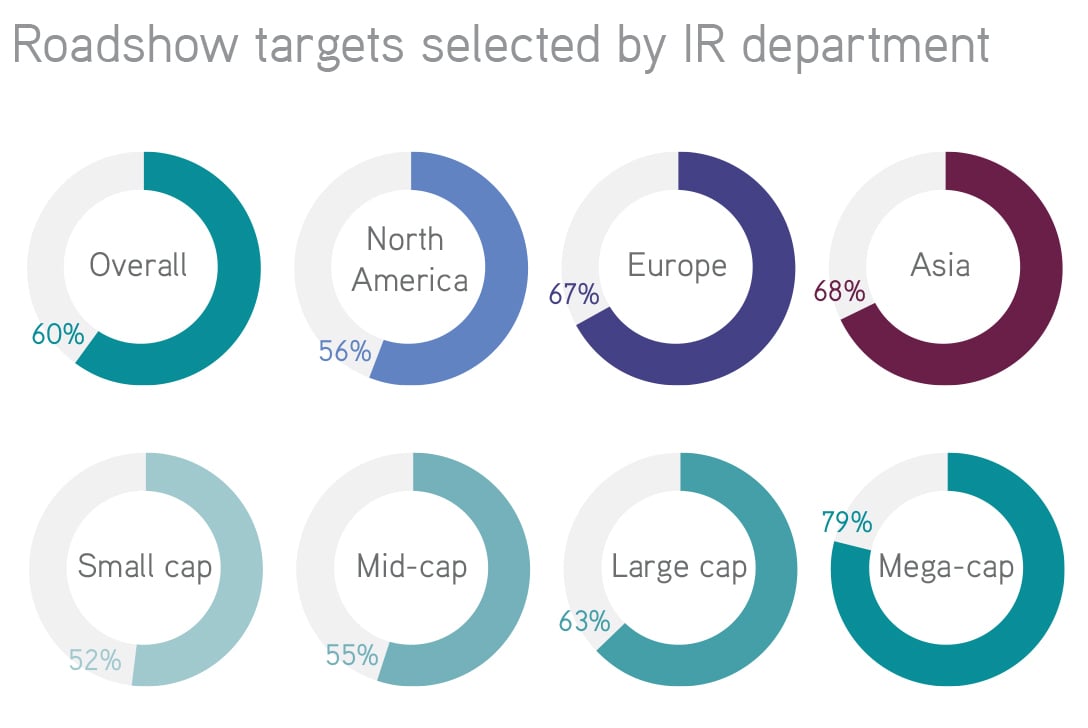

IR departments are having more say over who they meet on the road. Globally, six in 10 roadshow targets are selected by the IR team, an increase from 42 percent in 2017 and just over half in 2018.

This practice is even more common among European and Asian companies, where more than two thirds of roadshow targets are selected by the IR department. It is less common in North America, where slightly more than half (56 percent) of companies’ targets are selected by the IR team.

Direct targeting of investors for roadshows by the IR department increases with company size. Among small caps, 52 percent of targets are selected by the IR department. This number rises gradually though the cap sizes to 79 percent among mega-cap companies.

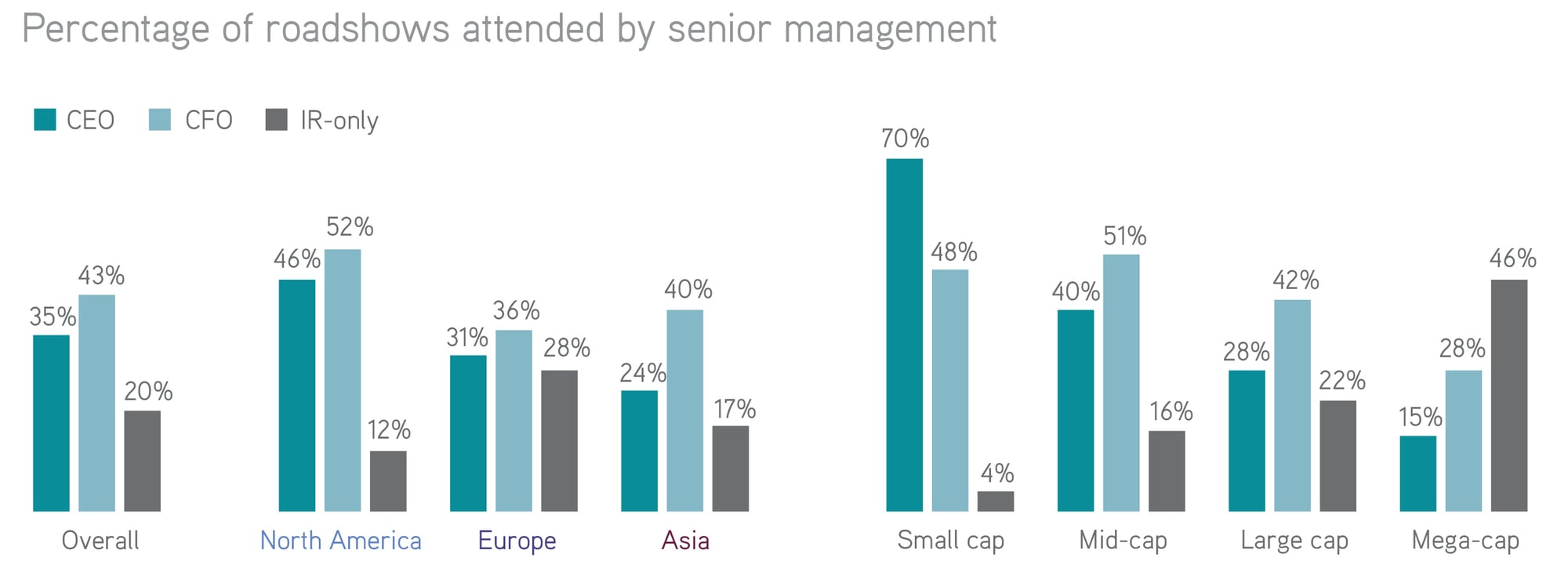

CFOs went on 43 percent of all roadshows globally in the past year, while chief executives participated in just over a third. This is a drop from the 2018 figures, when CFOs went on 44 percent of roadshows and CEOs went on 38 percent. Just one in five roadshows are conducted by IROs only with no senior management in attendance, down from 26 percent in 2018.

Regionally, more than half of all roadshows conducted by North American companies in the past year had a CFO in attendance, compared with 36 percent of roadshows by European companies and four in 10 of those conducted by Asian companies. North American CEOs are most likely to go on the road, while Asian chief executives participated in just one in four of their company’s roadshows in the past year. European companies are the most likely to go on the road without senior management, with 28 percent of their roadshows being IR-only.

The considerable gap between the percentage of roadshows attended by small-cap CEOs and mega-cap CEOs has widened even further in 2019. In the past year, CEOs at small-cap companies went on 70 percent of their company’s roadshows, up 6 percentage points from 2018. During the same period, mega-cap chief executives attended just 15 percent of their company’s roadshows, down from 19 percent the previous year.

Just 4 percent of small-cap roadshows were undertaken by the IR team alone, with no senior management in attendance. The proportion rises through the cap sizes to the point where 46 percent of mega-cap roadshows are undertaken by the IR team alone.

For this year’s roadshow report, we have looked at three areas that could influence roadshow activity and asked IR practitioners what impact they considered these areas to have had on their roadshow practice over the past three years. The areas we are examining here are increased use of technology, regulatory changes and the availability of online corporate access platforms.

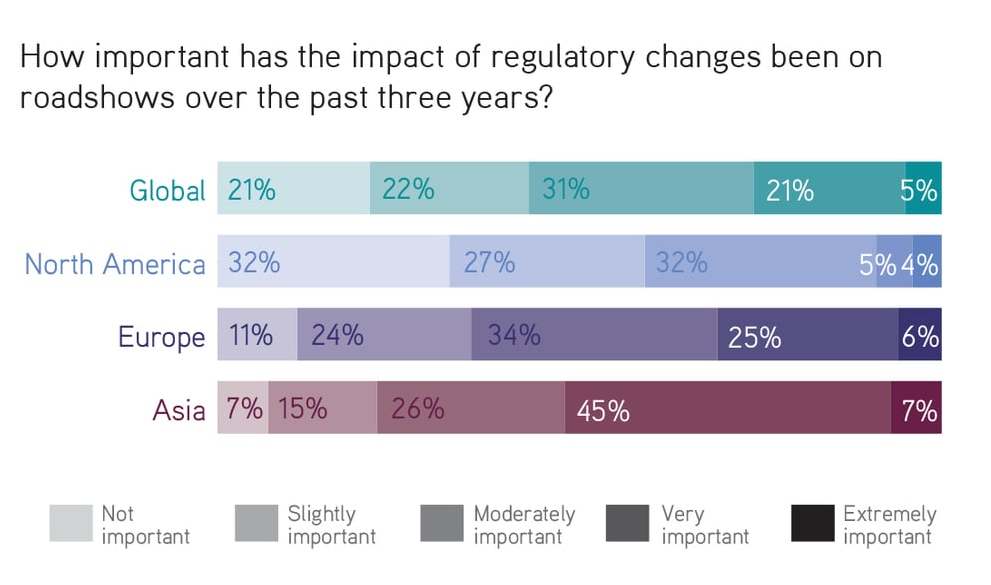

Regulatory changes have made a notable impact on roadshows over the past three years. Globally, more than a quarter of IR practitioners consider recent regulation to have had a very or extremely important impact on roadshow activity, while 57 percent view changes in regulation to be at least moderately important.

North American IROs are the least concerned about regulatory changes, with nearly a third considering the subject not important to their roadshow activity. On the other hand, more than half of Asian IROs consider new regulation to have had a very or extremely important impact on roadshow activity.

The view of regulatory changes being important to recent roadshow activity increases with company size: 21 percent of small-cap IROs consider them to be very or extremely important, rising to just under a third of IROs at mega-cap companies.

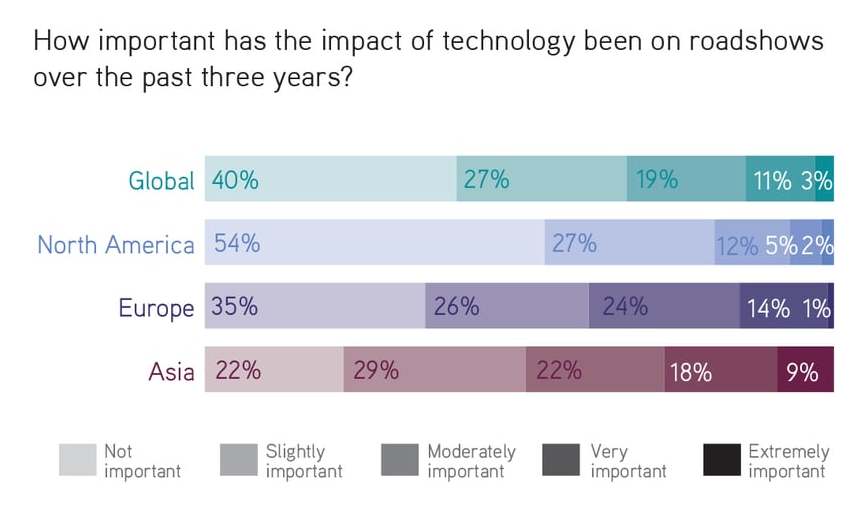

Overall, increased use of technology has not had a great impact on roadshow activity over the past three years. Just 14 percent of IR practitioners view the impact of technology as very or extremely important, with 33 percent seeing it as at least moderately important. Four in 10 IROs globally view the recent impact of technology as not important to roadshow activity.

Regionally, technology has had the least impact on roadshows in North America, where more than half view its impact as not important. Asian firms are the most affected, with almost half of IROs considering technology to be at least moderately important.

Nearly a quarter of IR practitioners at small-cap companies view the impact of technology on roadshows over the past three years as being very or extremely important. This compares with just one in 10 IROs at large-cap companies, where a further 46 percent see technology as not important to recent roadshow activity.

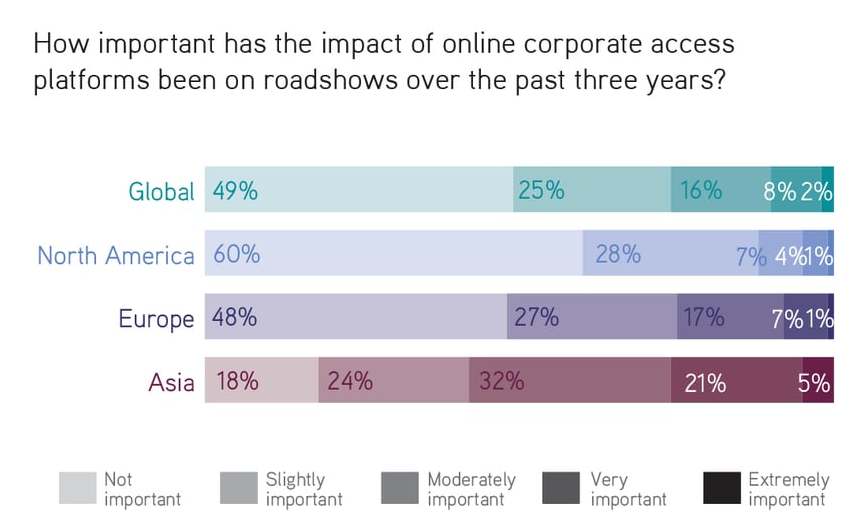

The past few years have seen a rise in the availability of online corporate access platforms, allowing IR departments to liaise directly with investors to arrange meetings and organize roadshow calendars. But these platforms do not appear to have changed roadshow activity in the past three years. Globally, just one in 10 consider them to have a very or extremely important impact on roadshows.

As with use of technology and regulatory changes, Asian IROs are those who see the greatest impact of corporate access platforms on roadshow activity, with 26 percent viewing them as either very or extremely important to this end. At the same time, six in 10 North American IROs see corporate access platforms as having no important impact on roadshows.

Just 6 percent of mega-cap IROs see the impact of corporate access platforms on roadshow activity as very important. The portion of IROs who consider them to have no impact on roadshows rises from 43 percent among small caps to six in 10 at mega-caps.